Weekly Trends

Trends based on more than 500,000 transactions per week. This public report only shows high level trends. For our participants we publish weekly data for hundreds of worldwide markets at different O&D levels.

- All

- 2023

- 2024

- 2025

- 2026

Hong Kong to Europe volumes slump as new EU rules kick in Air cargo tonnages…

China to Europe tonnages and spot rates drop sharply Worldwide air cargo tonnages and rates…

Rates fall further but the threat of renewed disruption returns Global air cargo average rates fell…

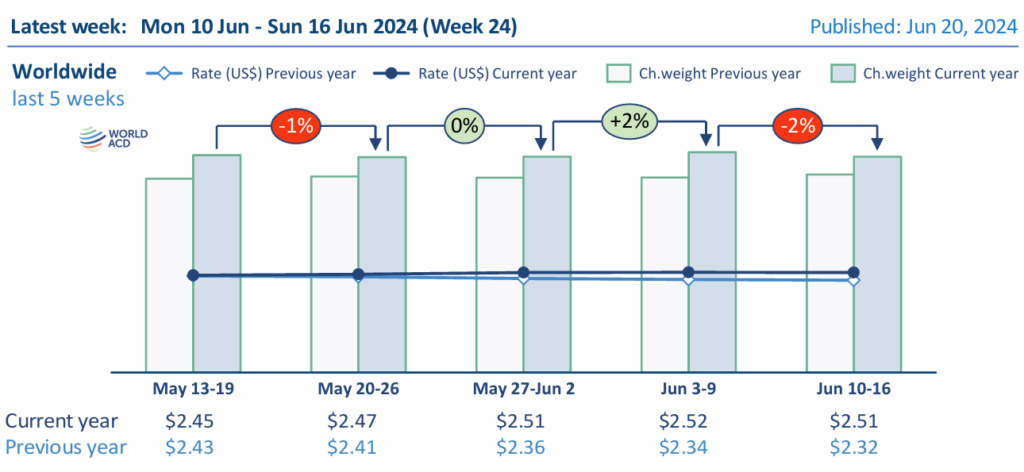

June tonnages up +9% on last year while spot rates slightly soften Worldwide air cargo…

Rates stay high despite further capacity returning to Gulf markets Worldwide and regional air cargo…

Market shows signs of stability Despite a temporary flare-up of the conflict in the Middle…

Volumes and capacity recover from holiday contraction Air cargo activity stepped up a gear and…

Holidays slow traffic but not pricing Global traffic volume in terms of chargeable weight dropped…

Worldwide tonnages and rates stabilize Worldwide air cargo markets appear to have broadly stabilized in…

Asia Pacific tonnages rebound as stability returns to some markets Air cargo tonnages from…

Tonnage, pricing and capacity in decline In the first full week of May airfreight retreated…

Tonnage rebounds to +5% in April, end of flower surge After several weeks of growth…

Flower shipments boost global tonnages, rates edge further upwards Worldwide air cargo capacity and tonnages…

Rate increase slows as Middle East capacity further rebuilds The steep rise in average global…

Rates rise further despite drop in worldwide tonnages Global air cargo rates have continued to…

Traffic slowdown does not halt rising rates With the exception of the Middle East and…

Prices reach new highs even as traffic growth stalls Even though the rebound in global…

Rates rise further as markets continue to adjust to the Iran war Global air cargo…

Rates continue rising amid partial recovery of Gulf capacity Air cargo spot rates are continuing…

Rates jump as capacity and traffic are hit by Iran war repercussions Data of the…

Assessing the impact of the Iran War on airfreight flows The attacks on Iran by…

Tonnages nosedive due to Lunar New Year Worldwide air cargo tonnages plummeted in mid-February, largely…

Global tonnage turns negative after weeks of growth Seasonal events are impacting air cargo traffic…

Global tonnages rise further after Valentine’s Day flower peak Global air cargo demand and rates…

Market remains steady in lead up to Lunar New Year Worldwide air cargo demand rose…

Demand stabilizes ahead of Lunar New Year Global air cargo demand and prices have broadly…

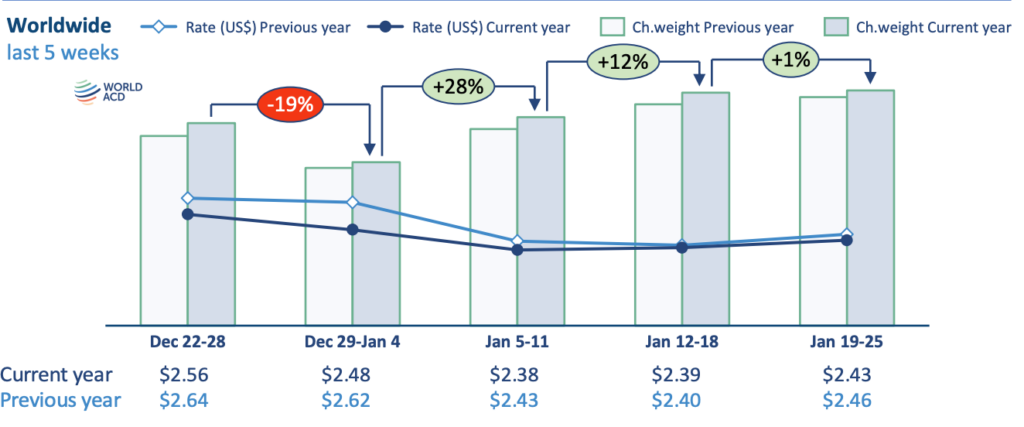

Tonnages rebound further as 2026 gathers momentum Worldwide air cargo volumes continued to recover strongly…

Demand rebounds after normal end-of-year slump Global air cargo tonnages rebounded strongly in the first…

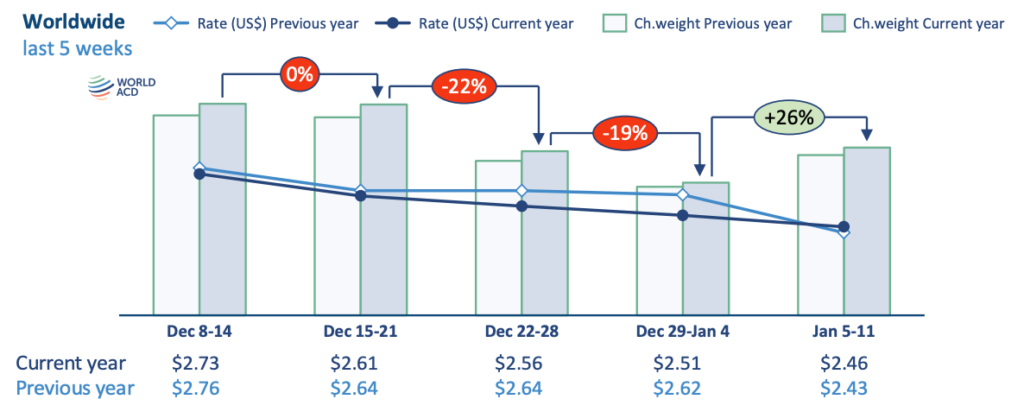

Revenues rise +3% in 2025 as tonnages grow to new record Worldwide total air cargo…

Tonnages peak and rates approach last year’s highs Worldwide air cargo tonnages edged back downwards…

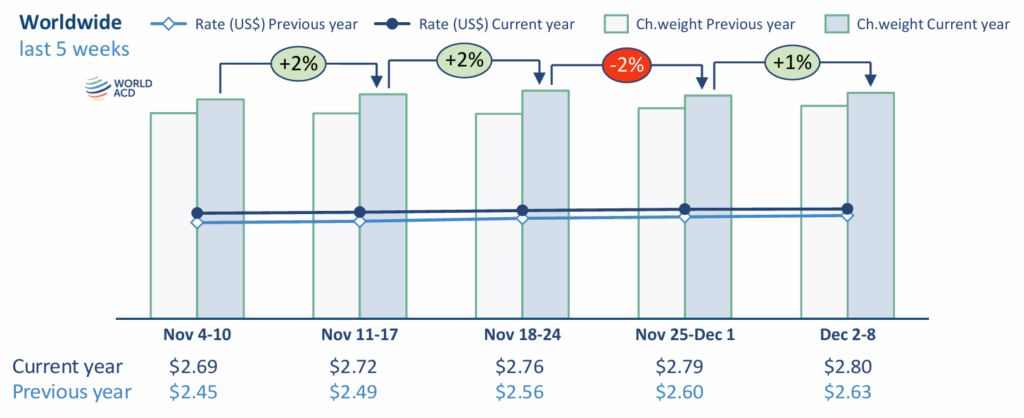

Spot rates rise a further +3% in first week of December International air cargo spot…

November tonnages up +5% on last year Worldwide air cargo tonnages in November continued their…

Spot prices edge higher in end-of-year build-up Air cargo spot rates globally, and from Asia…

Rates continue rising as Southeast Asia to US demand booms Air cargo rates have continued…

Asia Pacific spot rates continue to rise Air cargo spot rates from Asia Pacific origins…

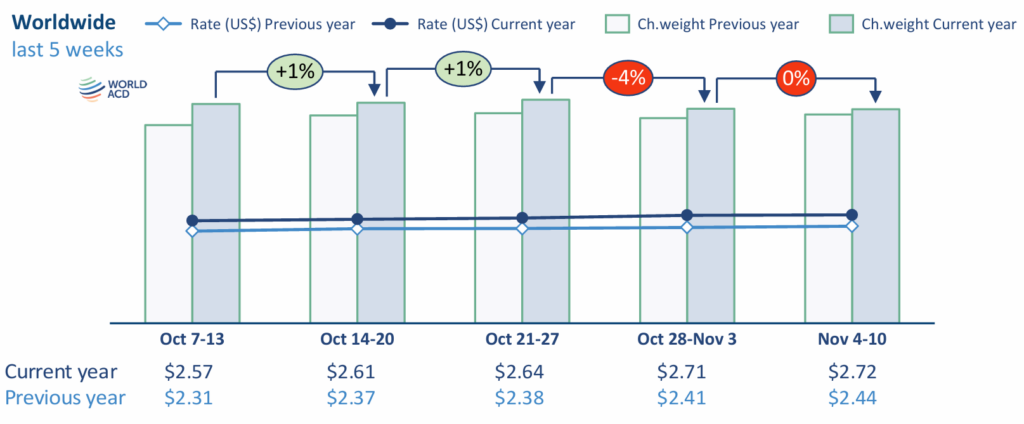

Tonnages on track for +4% growth this year Worldwide air cargo tonnages are on track…

Spot rates gaining momentum ahead of peak season Worldwide average spot rates surged in the…

Worldwide tonnages rebound +6% from Asia holiday lull Global air cargo tonnages rebounded with a…

Holiday season in Asia holds back worldwide tonnages Worldwide air cargo tonnages dropped -3% in…

Tonnages rebound from Hong Kong and China following typhoon Air cargo tonnages from Hong Kong…

Tonnages grow +4% in the third quarter of 2025 Worldwide air cargo tonnages were up…

Rates edge upwards, but deficit widens with last year Worldwide average air cargo rates edged…

India to USA tonnages continue to fall despite wider volume rebound Air cargo tonnages from…

India to USA air exports plummet as higher tariffs take effect Air cargo exports from…

August figures point to structural shift from China-USA to China-Europe markets The full-month figures for…

Global tonnage rebounds following Japanese holidays Air cargo tonnage out of Asia Pacific jumped +8%…

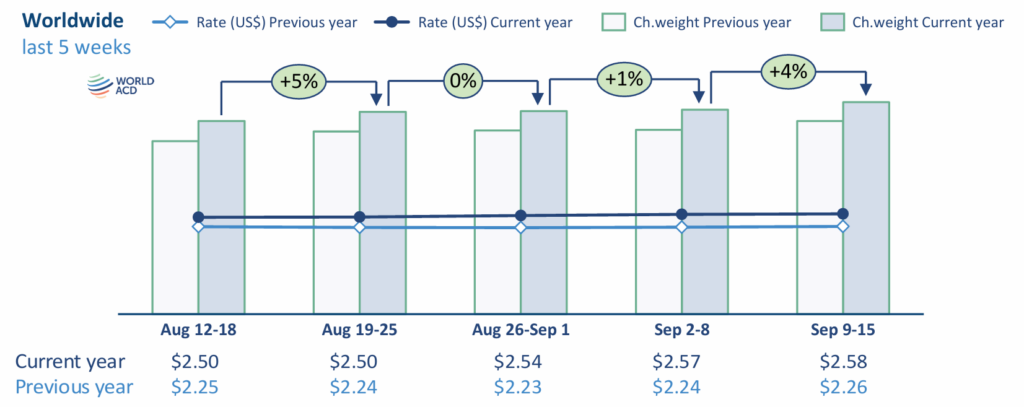

Japanese and European holidays lead to mid-August tonnage drop National holidays in Japan and several…

Global tonnage slows further as rates gradually increase Global airfreight tonnage retreated for a second…

July shows rebound in tonnages while rates remain under pressure July closed out with a…

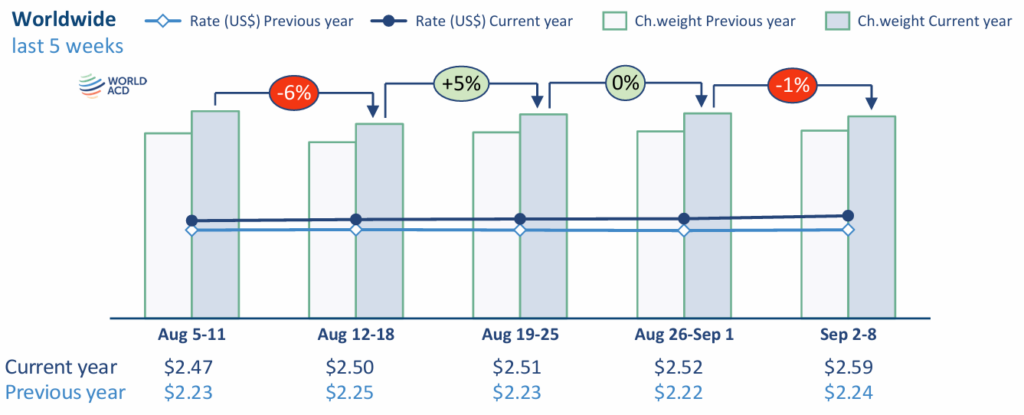

Hong Kong to US tonnages rebound after Typhoon Wipha Air cargo tonnages from China and…

Markets soften slightly as 1 August US tariff deadline looms Air cargo tonnages softened in…

Asia Pacific to US tonnages fall further Worldwide air cargo rates held firm in the…

Demand dips due to US Independence Day, in another turbulent week Worldwide air cargo demand…

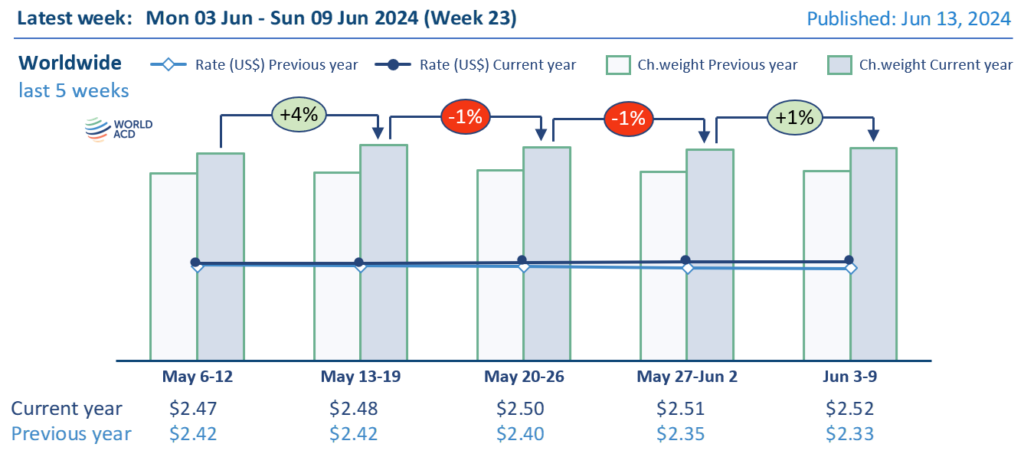

Rates edge upwards +2% in June amid volatile markets Average worldwide air cargo rates rose…

Middle East & South Asia tonnages partially rebound Air cargo tonnages from Middle East &…

Middle East & South Asia tonnages recover slowly after Eid Air cargo traffic to and…

China to US tonnages and rates weaken again After rebounding in the latter part of…

Worldwide tonnages rebounded +4% in May Worldwide air cargo tonnages rebounded in May with a…

Global air cargo market stable, while China to USA lane recovers The air cargo market…

Asia Pacific and worldwide tonnages rebound Worldwide air cargo tonnages rebounded substantially last week with…

Demand drops further in the wake of 'de minimis' exemption end Worldwide chargeable weight declined…

Labor Day adds to tonnage declines from Asia Pacific Air cargo tonnages declined steeply last…

Worldwide tonnages up +6% in April, year on year Preliminary air cargo figures for April…

Rates from Asia Pacific fall further amid market uncertainty Air cargo markets from Asia Pacific…

Post-Eid recovery masks downward pressure on demand Global tonnage improved +3% in week 15 (April…

Tonnages drop due to Eid and growing global uncertainty The slowdown in global tonnage that…

First quarter 2025 up +3%, ahead of new US tariffs Worldwide air cargo tonnages grew…

China to USA spot rates rebound Average worldwide air cargo rates regained a further +4%…

Rates and demand continue on slight upward trend Global air cargo rates and demand edged…

Flat markets slightly above last year’s levels Worldwide air cargo markets show a flat trend…

China to USA market weakens in February Full-month figures for February suggest a weakening China…

Asia Pacific tonnages are close to pre-Lunar New Year levels Air cargo tonnages from Asia…

Slow recovery continues from Lunar New Year Worldwide air cargo tonnages have continued to recover…

Demand rebounds slightly from Lunar New Year dip Global air cargo tonnages rebounded slightly (+3%)…

Tonnage growth eases in January ahead of early Lunar New Year Worldwide air cargo recorded…

Rates rebound in lead-up to Lunar New Year Average global air cargo rates have edged…

Demand edges back upwards ahead of Lunar New Year break Worldwide air cargo tonnages continued…

Asia rates remain high despite seasonal slowdown Global air cargo spot prices remain more than…

Softening growth in tonnages and rates Worldwide air cargo finished the year at its lowest…

Tonnages and rates begin dropping after strong Q4 peak Air cargo’s strong seasonal fourth quarter…

Asia Pacific spot rates continue rising into December Global air cargo average spot rates rose…

Rates rise to a 2024 high in November, despite dip in tonnages Worldwide air cargo…

Tonnages hold firm while rates continue to build in peak season Global tonnages in the…

Rates spike from Europe to Americas lifts global prices A sharp rise in air cargo…

Spot rates rise further as peak season builds Worldwide air cargo average spot rates have…

Asia Pacific and Europe rate rises lift global prices Rising air cargo rates from Asia…

Rates rise further in last full week of October Average worldwide air cargo spot rates…

Hong Kong to Europe tonnages continue to build Air cargo tonnages from China to Europe…

China-USA tonnages remain depressed after Golden Week Worldwide and Asia Pacific air cargo tonnages have…

Rates rise to 2024 high despite tonnage dip Global air cargo spot rates rose to…

Rates and demand rise further in September as strong peak looms Worldwide air cargo rates…

Autumn festivals cause mid-September dip in tonnages from Asia Pacific Global air cargo tonnages dipped…

Bangladesh and Japan rates soar as disruptions persist Soaring air cargo spot rates from Bangladesh…

Asia Pacific surge lifts global rates Worldwide average air cargo spot rates rose to a…

Rates and demand remain strong throughout August Worldwide air cargo demand and pricing have stayed…

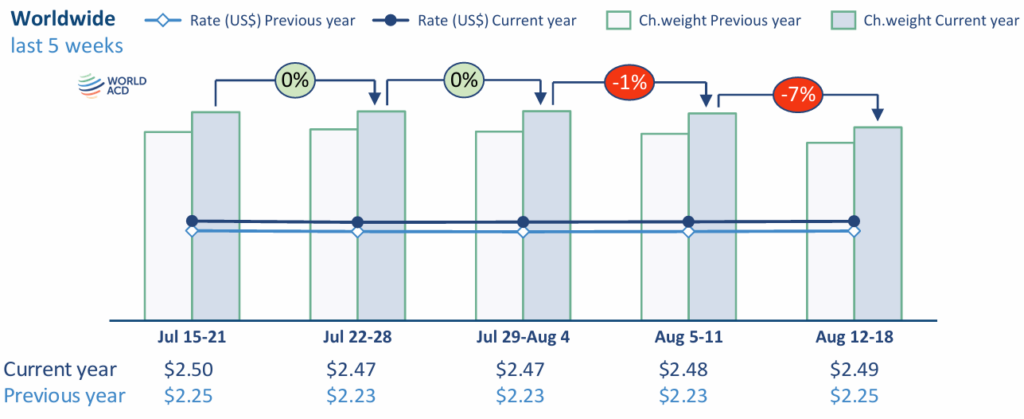

Asia Pacific tonnages rebound strongly after Japan typhoon dip Air cargo tonnages from Asia Pacific…

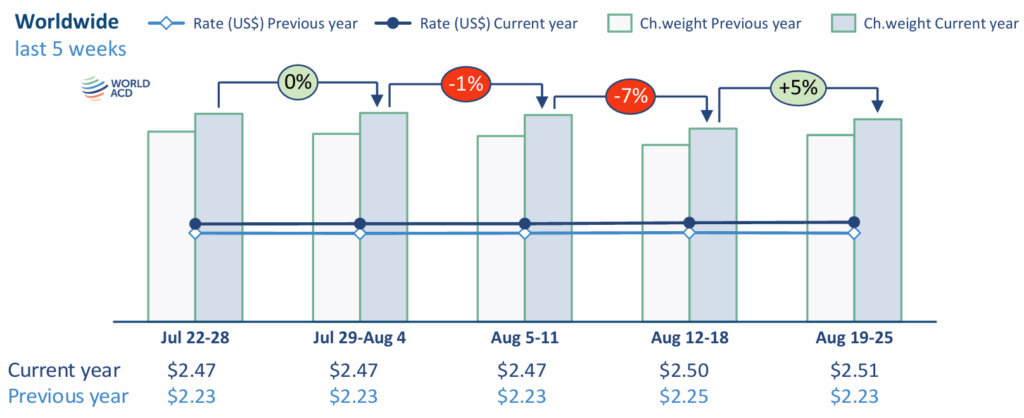

Japan typhoon and European holidays cause mid-August tonnage drop Flight cancellations caused by a typhoon…

Rates hold firm while tonnages weaken slightly at the start of August Average worldwide…

Tonnages and rates up +12% in July, Bangladesh tonnages recover Average worldwide air cargo rates…

Bangladesh disruptions contribute to stalling tonnages in late July Worldwide air cargo tonnages remained flat…

Asia Pacific rates soar despite drop in China-USA demand Air cargo spot rates from Asia…

Rates stay firm despite slight July demand lull Worldwide air cargo rates and demand softened…

Demand dips due to US Independence Day, rates stay high ex-Asia Global air cargo demand…

Tonnages up +12% in the first half of 2024 Global air cargo tonnages were up…

Global tonnages dip due to Eid al-Adha festival Worldwide average air cargo rates have continued…

Rates stay firm driven by Asia and Middle East Air cargo rates are holding firm…

Asia Pacific demand and rates soar above last year’s levels Air cargo demand and rates…

Rate surge continues throughout May from Middle East & South Asia Air cargo rates from…

Global rates stabilize above last year's levels Global air cargo rates have been gradually increasing…

Rates and tonnages from Middle East and Asia remain high Air cargo tonnages and rates…

Asia Pacific tonnages partially rebound following Labour Day dip Air cargo demand from Asia Pacific…

Tonnages dip due to Labour Day holidays Worldwide air cargo tonnages dipped in the week…

Tonnage surge continues from Central & South America Air cargo tonnages from Central & South…

Mother’s Day flower shipments boost global tonnages Global air cargo tonnages returned to growth in…

Eid weakens demand but rates hold firm Following successive weekly rises since the end of…

Rate rise continues into April as South Asia-Europe rates soar Worldwide air cargo rates have…

Global rates rise throughout March to Q4 levels Global air cargo rates continued to rise…

Rates continue to rise from Asia and Middle East & South Asia Air cargo rates…

Asia Pacific export tonnages and rates continue to rise Air cargo tonnages and rates from…

Dubai-Europe tonnages continue surge, as global demand stabilizes Air cargo tonnages from Dubai to Europe…

Tonnages up +13% in first two months of 2024 Worldwide air cargo demand was up…

Tonnages rebound post-LNY as sea-air surge continues Global air cargo tonnages have rebounded in the…

Asia-Europe sea-air hubs record strong surge in tonnages Several key Asia-Europe sea-air hubs have recorded…

China inbound tonnages slump as Year of the Dragon starts China’s air import tonnages dropped…

Ex-China rates surge ahead of Lunar New Year Air cargo rates from China have surged…

Tonnages build ahead of Lunar New Year Global air cargo tonnages continued to build in…

January tonnages well up on last year’s levels Worldwide air cargo demand in January so…

Volumes bounce back after New Year slowdown Global air cargo tonnages have bounced back in…

Uncertain start to 2024 Worldwide air cargo tonnages dropped further in the first week of…

Full year 2023 ends at -5%, year on year Global air cargo has yet to…

Tonnages in Q4 2023 closing at +3% Year-on-Year With the year 2023 coming to an…

Rates bounce back to +50% above pre-Covid level Global average air cargo rates now stand…

Peak-season tonnages up 3% on last year Worldwide air cargo demand has rebounded significantly above…

Rates ex-Asia Pacific continue strong rise Global air cargo tonnages have rebounded more quickly than…

Thanksgiving tonnage decline less severe than last year Worldwide air cargo demand patterns have continued…

Q4 demand so far exceeds last year’s levels Global air cargo demand in the fourth…

Rates continue upward trend while tonnages stabilize Worldwide average air cargo prices have continued their…

Rates hold firm despite early November tonnage dip Global average air cargo rates have remained…

October tonnages track close to last year’s levels Global air cargo tonnages stabilized in October…

Tonnages and rates stabilize after recovery from Golden Week Global air cargo tonnages and rates appear…

Tonnages partially recover from China’s Golden Week Global air cargo tonnages recovered slightly in the…

Golden Week pushes down early October tonnages Global air cargo tonnages dropped significantly in the…

Tonnages and rates rise in September Global air cargo tonnages and average rates have risen…

Continuing rise for rates and tonnage Global air cargo tonnages and average rates have continued…

Tonnages fall further while rates hold firm Average global air cargo rates have stabilized in…

Sign up for our Trends messages.

"*" indicates required fields

Interested to learn more

Complete the form to receive more info or to plan an online demo.

"*" indicates required fields