Air Cargo market trends

As an important partner for Airlines, Forwarders, Shippers, Airports and GSAs, our detailed weekly and monthly data allow a quick response to market dynamics. Besides the datasets that we make available to our customers, we also publish a few regular reports with high level trends for the air cargo industry. You can read and download these reports below.

Weekly trends

Charts with the Weekly trends

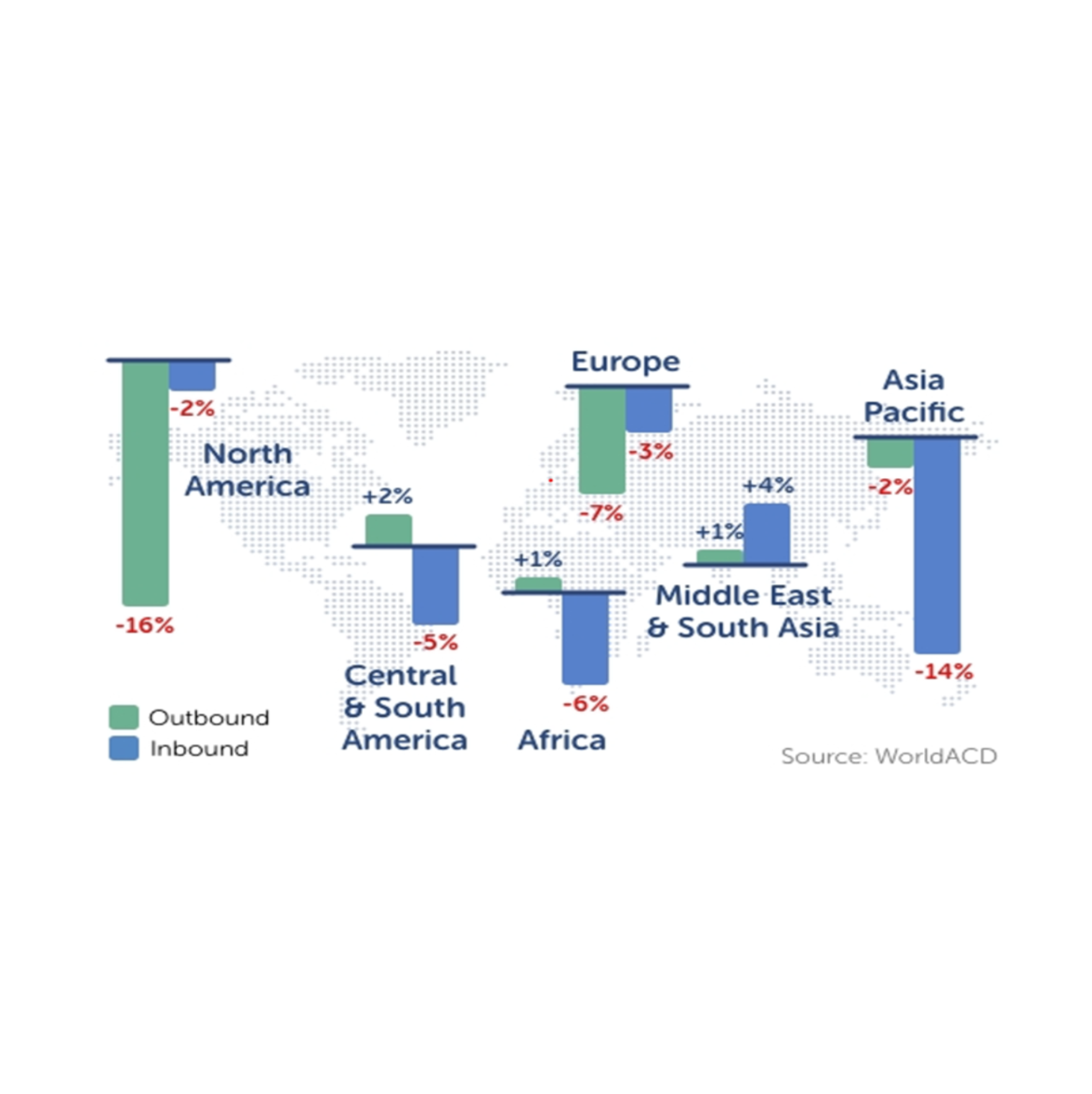

Monthly trends

Charts with the Monthly trends

Index charts

Charts regarding the Index

Yields/Rates

Charts regarding the Yield/Rates

Peek of the Week

Charts regarding specific Air Cargo insights

Latest trends in your mailbox?

Sign up for our Trends messages.

Interested to learn more

Complete the form to receive more info or to plan an online demo.

"*" indicates required fields